TK-GK scheme

目次

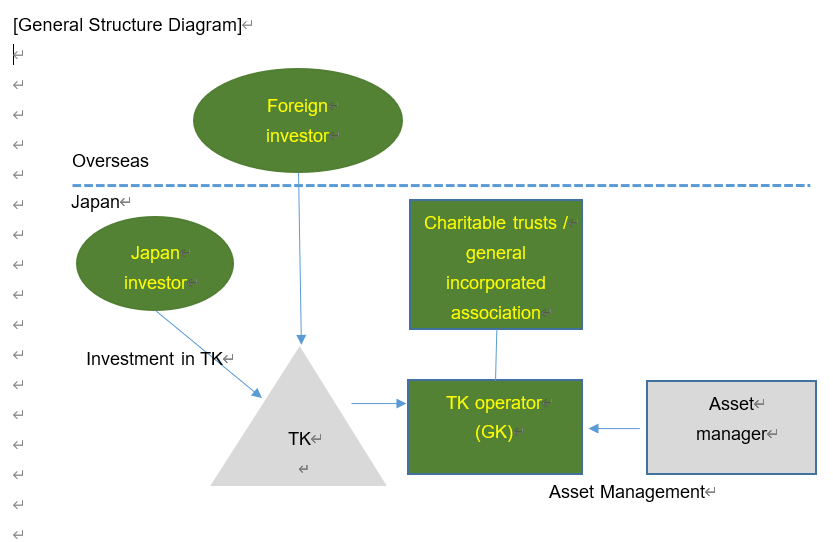

Overview

Silent Partnership (Tokumei Kumiai (TK)) and Limited Liability Company (Godo Kaisha (GK)) Structure is the most popular investment scheme for real estate and renewable energy, etc. is a “TK-GK structure”.

Legal character

- A TK is a contract stipulated in the Japanese Commercial Code, under which TK investors are entitled to contribute funds to TK operators and receive distributions of profits generated from TK activities.

- A TK investors’ liability is limited to the amount invested.

- TK investors have no right to be involved in the operations of the TK.

Japanese taxation of TK

- TK operators recognize all revenues and expenses arising from TK activities. In calculating the TK operator’s taxable income, the profits distributed to the TK operator are deducted from the TK operator’s taxable income, and the losses distributed to the TK operator are added to the TK operator’s taxable income. This treatment does not require actual cash transfer of profits or the burden of losses (Basic Coporate Tax Cirucular 14 -1 -3).

- The distribution of profits to TK investors is subject to Japanese withholding tax at a rate of 20.42%.

- TK investors (assuming they are corporations) are taxed on the profits distributed by TK operators. Withholding tax withheld by TK operators can be credited against corporate tax of TK investors.

Japanese taxation of foreign TK investors

- TK operators recognize all revenues and expenses arising from TK activities. In calculating the TK operator’s taxable income, the profits distributed to the TK operator are deducted from the TK operator’s taxable income, and the losses distributed to the TK operator are added to the TK operator’s taxable income. This treatment does not require actual cash transfer of profits or the burden of losses (Basic Coporate Tax Cirucular 14 -1 -3).

- The distribution of profits to TK investors is subject to Japanese withholding tax at a rate of 20.42%.

- There is a risk that the TK may be treated as a general partnership if the TK investor is involved in the TK business. If there is a general partnership in Japan, the foreign investor would be deemed to have a permanet establishment (“PE”) in Japan. If a PE is created in Japan, the foreing investor would be subject to 30% corporate tax. Note that in past tax audits, the National Tax Agency denied the existence of a TK contract and asserted that there was a general partnership.

We would recommend discussing with a tax expert who is familiar with TKs before implementing such a structure.

投稿者プロフィール

- 税理士

-

湘南地区の国際税理士です。藤沢市在住。東京、神奈川を中心に活動しています。トーマツに20年在籍、ニューヨークにも駐在していました。

I am a tax accountant. My name is Tomotaka Kuwata. I have worked for Deloitte Tohmatsu for 20 yeas and seconded to Deloitte New York. My office is in Yokohama. Please feel free to contact me.

最新の投稿

English2022.06.22Japan corporate tax overview

English2022.06.22Japan corporate tax overview English2022.06.18Godo Kaisha

English2022.06.18Godo Kaisha English2022.06.17Sole proprietor VS company

English2022.06.17Sole proprietor VS company English2022.06.17Blue Tax Payer Benefits

English2022.06.17Blue Tax Payer Benefits